Children Pensions/Investments

The younger generation face a great deal of financial pressure as they get older, so giving their pension a boost now could be extremely helpful.

A child pension also known as Junior SIPP can be opened on behalf of a child from the day they are born until they reach the age of 18. Junior SIPPs are a very tax-efficient way of saving and the money is locked away safely so the child usually can't withdraw until they reach the age of 55.

Parent(s)/guardian(s) can contribute a maximum of £2,880 per year (topped up to £3,600 by the government) until the age of 18. Once the child reaches the age of 18, control will be passed on to them and they can then choose to start making personal contributions themselves or let the money sit.

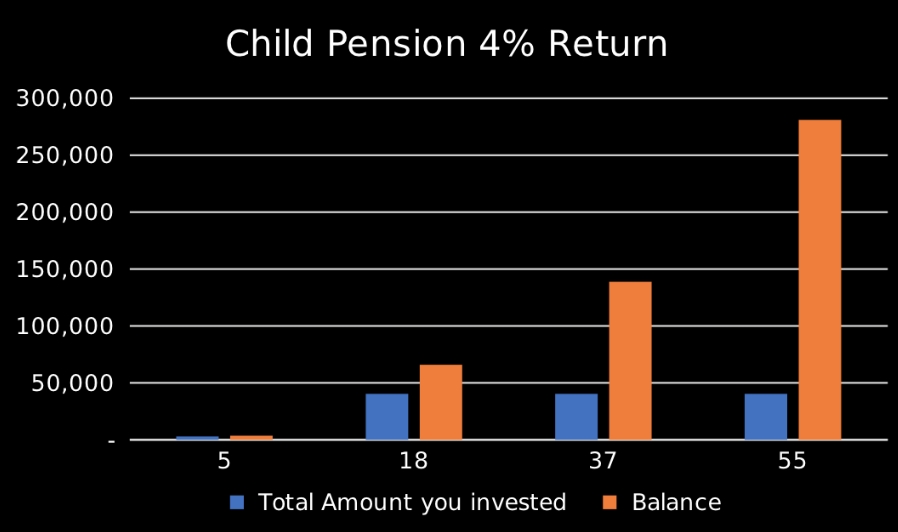

Below you will find a chart which shows a child pension account opened at the age of 5 and parent(s)/guardian(s) contributing £2,880 per year until the age of 18. Once the child reaches the age of 18, the child will have an account worth £65,851*.

The child, now adult decides not to touch his pension amount and leaves the £65,851* to grow until the age of 55. At the age of 55, it will be worth £ 281,057* costing you only £40,320.

The value of investements and the income they produce can fall as well as rise. You may get back less than you invested. Tax treatment varies according to individual circumstances and is subject to change.

*Based on a 4% annual return

Invest £2.8k a year for 13 years

Given £0.8k a year by Government for 13 years.

5% per annum assumed growth

Over a period from 5 age to 55 age (50 years). this would achieve £240k. Being £237k profit/gain.

This is a fictional example which was created for illustrative purposes only.